Financial Management for Small Businesses, 2nd OER Edition

Financial Management for Small Businesses, 2nd OER Edition by Lindon J. Robison is licensed under a Creative Commons Attribution 4.0 International License, except where otherwise noted.

Financial Management for Small Businesses

Financial Statements & Present Value Models

Second Open Edition

Lindon J. Robison

Steven D. Hanson

J. Roy Black

2021

East Lansing, MI

Financial Management for Small Businesses, 2nd OER Edition by Lindon J. Robison is licensed under a Creative Commons Attribution 4.0 International License, except where otherwise noted.

1

We dedicate this book to all the students of Agribusiness Management ABM 435 at Michigan State University who over the years have challenged us to increase our understanding of and to improve the presentation of financial management concepts.

2

FINANCIAL MANAGEMENT FOR SMALL BUSINESSES:

Financial Statements & Present Value Models

Second Open Edition

Written by:

Lindon J. Robison

Steven D. Hanson

J. Roy Black

Agricultural, Food and Resource Economics

Michigan State University

East Lansing, Michigan

United States of America

© 2021 Lindon J. Robison

Financial Management for Small Businesses: Financial Statements & Present Value Models by Lindon J. Robison is licensed under a Creative Commons Attribution 4.0 International License.

Garden center photo on cover by Liz West. Used under the Creative Commons Attribution 2.0 Generic License.

Farm field photo on cover by Ryan Vroegindewey. Used under the Creative Commons Attribution 2.0 Generic License.

Main Street photo on cover by Loren Shattuck. Used under the Creative Commons Attribution 2.0 Generic License.

Cover and interior design by Julie Taylor.

3

A: constant loan payment

AE: annuity equivalent

AIS: accrual income statement

AL: accrued liabilities

AP: accounts payable

APR: annual percentage rate

AR: accounts receivable

ATCF: after-tax cash flow

AVG: attachment value goods

CA: current assets

CE: cash expenses

CFS: coordinated financial statements

CL: current liabilities

COGS: cost of goods sold

CPI: consumer price index

CR: cash receipts

d: geometric decay

D: debt

Dep: depreciation

E: equity

EBIT: earnings before interest and taxes

EBT: earnings before taxes

EV: expected value-variance

FTC: Federal Trade Commission

FV: future values

g: nominal growth rate

g*: real growth rate

GAAP: generally accepted accounting practices

i: average interest rate

i (superscript): investment identifier

INV: inventories

IRR: internal rate of return

IRRA: internal rate of return on Assets

IRRE: internal rate of return on Equity

IRS: Internal Revenue Service

L: loan amount

LLC: Limited Liability Company

m: profit margin

MACRS: modified accelerated cost recovery system

MIRR: modified IRR

mn: term

MNPV: modified NPV

NIAT: net income after taxes

NPC: net present cost

NPV: net present value

NPVA: NPV for asset earnings

NPVE: NPV for equity earnings

NWC: net working capital

OE: overhead expense

p: percent of loan to be paid as a refinance cost

PV: present value

QTM: quantity theory of money

r: nominal discount rate

rf: APR

rm: market rate of interest

r*: real discount rate

R: constant value of net cash flow

constant value of cash deposits

Rti: cash flow earned by investment i in the tth period

R (bold): vector of cash flow values Rti earned by V0i

RCG: Realized Capital Gains

ROA: return on assets

ROE: return on equity

ROI: return on investment

S: units sold, liquidation value, sum of compounded periodic cash flows, standard deviation from a sample distribution

SCF: statement of cash flow

SEC: Securities and Exchange Commission

SEG: socio-emotional goods

T: tax

t (subscript): time period

TI: total interest

V0: initial value

W: firm’s wealth value

w: outcome variable

WCC: Weighted Cost of Capital

y: outcome variable

FV: future value

IPMT: interest payment

IRR: internal rate of return

NPER: number of periods

NPV: net present value

PMT: period payment

PV: present value

RATE: rate

Cov(): covariance

E(): expected value operator

Pr(): probability

(r, Rti): Sum of periodic cash flows

US0(rf/m, mn): uniform series of $1 payments discounted at the actuarial rate for (mn) periods

α (alpha): endogenous projection constant; tax adjustment rate for capital gains (losses)

β (beta): coefficient multiplying an exogenous variable

γ (gamma): scaling factor; rate of technological change; financed proportion of the purchase price; percentage between 0 and 100; change in L0; % of the investment’s value allowed to be deducted in a given year

∆ (Delta): difference / change

δ (delta): compounding / discounting factor; percent compensation for lost revenues

ϵt (epsilon): average error in the tth period

ϵ (epsilon): random variable component of a risky event

η (eta): capital gains (loss) rate

θ (theta): average tax adjustment coefficient

λ (lambda): average risk aversion coefficient

μ (mu): the expected value of a probability density function

π (pi): insurance premium paid to exchange a risky distribution with a sure value

ρ (rho): correlation coefficient between two random variables

σ (sigma): variance of a probability density function

ATO: asset turnover ratio

ATOT: asset turnover time ratio

C: coverage ratio

CT: current ratio

CTR: current-to-total returns ratio

DE: debt-to-equity ratio

DS: debt-to-service ratio

EM: equity multiplier ratio

ITO: inventory turnover ratio

ITOT: inventory turnover time ratio

PE: price-to-earnings ratio

PTO: payable turnover ratio

PTOT: payable turnover time ratio

QK: quick ratio

RTO: receivable turnover ratio

RTOT: receivable turnover time ratio

SPELL: solvency, profitability, efficiency, liquidity, leverage

TIE: times interest earned ratio

4

Financial Management and the Firm

Managing Risk

System Analysis

Incremental Investments

Forecasting and Present Value Models

Homogeneous Liquidity and Currency

Loan Analysis

Land Investments

Financial Investments

Yield Curves

Econs and Humans

Appendix

5

Tables that use Microsoft Excel formulas include a link to open the corresponding Excel spreadsheet.

Templates

Alternative Forms of Business Organizations

The Federal Tax System

Managing Risk

Financial Statements

Financial Ratios

System Analysis

Present Value Models and Accrual Income Statements

Present Value Models

Incremental Investments

Forecasting and Present Value Models

Homogeneous Sizes

Homogeneous Terms

Homogeneous Liquidity and Currency

Loan Analysis

Land Investments

Leases

Financial Investments

Yield Curves

Econs and Humans

6

This book intends to help students and others learn how to successfully manage the finances of small to medium-size firms. The underlying assumption of this book is that successful financial managers need to master the construction and analysis of financial statements and present value models. Learning how to construct and analyze financial statements and present value models is the focus of this book that is divided into five parts.

The chapters in Part I introduce management. Chapter 1 describes the firm management process—a process that includes identifying the firm’s mission statement and strategic (long term) goals and tactical (short term) objectives; identifying the firm’s strengths, weaknesses, opportunities, and threats; identifying and evaluating alternative strategies; and finally implementing and evaluating the preferred strategy. Chapter 1 notes that the management process has wide application including managing the financial resources of the small to medium-size firm.

The firm’s opportunities and threats are most often nested in factors outside the firm’s control. For example, different ways to organize the firm (Chapter 2) and the tax environment facing the firm (Chapter 3) are factors external to the firm. They are important to discuss, though, because the firm can adopt different responses to the legal and tax environment in which it operates.

We live in and make financial decisions in a world of risk and uncertainty. So how do we make choices when we can’t be certain what the outcomes will be? Formal insurance programs are one way of addressing the risk firms face. However, there are other risk responses the firm can employ. Learning about risk and applying this knowledge to the purchase of insurance and adopting other risk management alternatives is the focus of Chapter 4. Some of the concepts covered in Chapter 4 are essential statistical tools needed to plan and make important decisions in a risky and uncertain world.

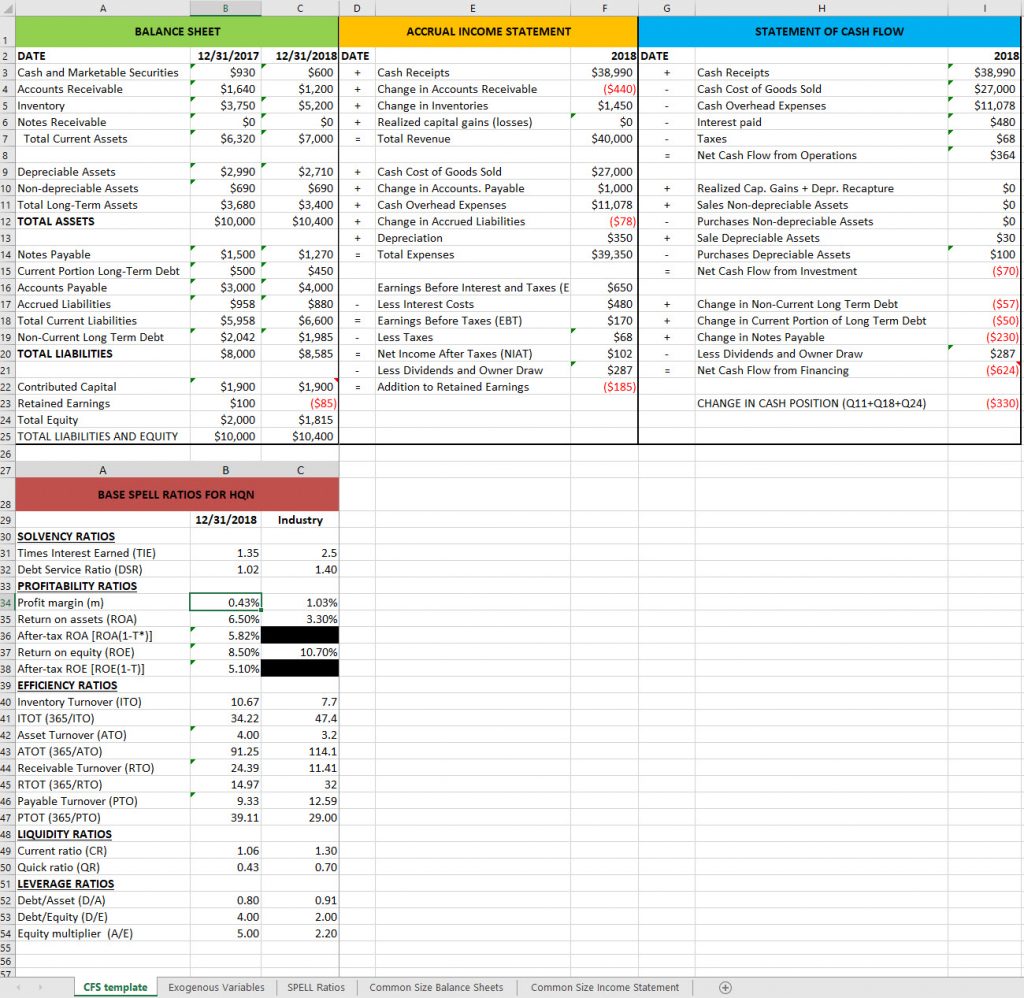

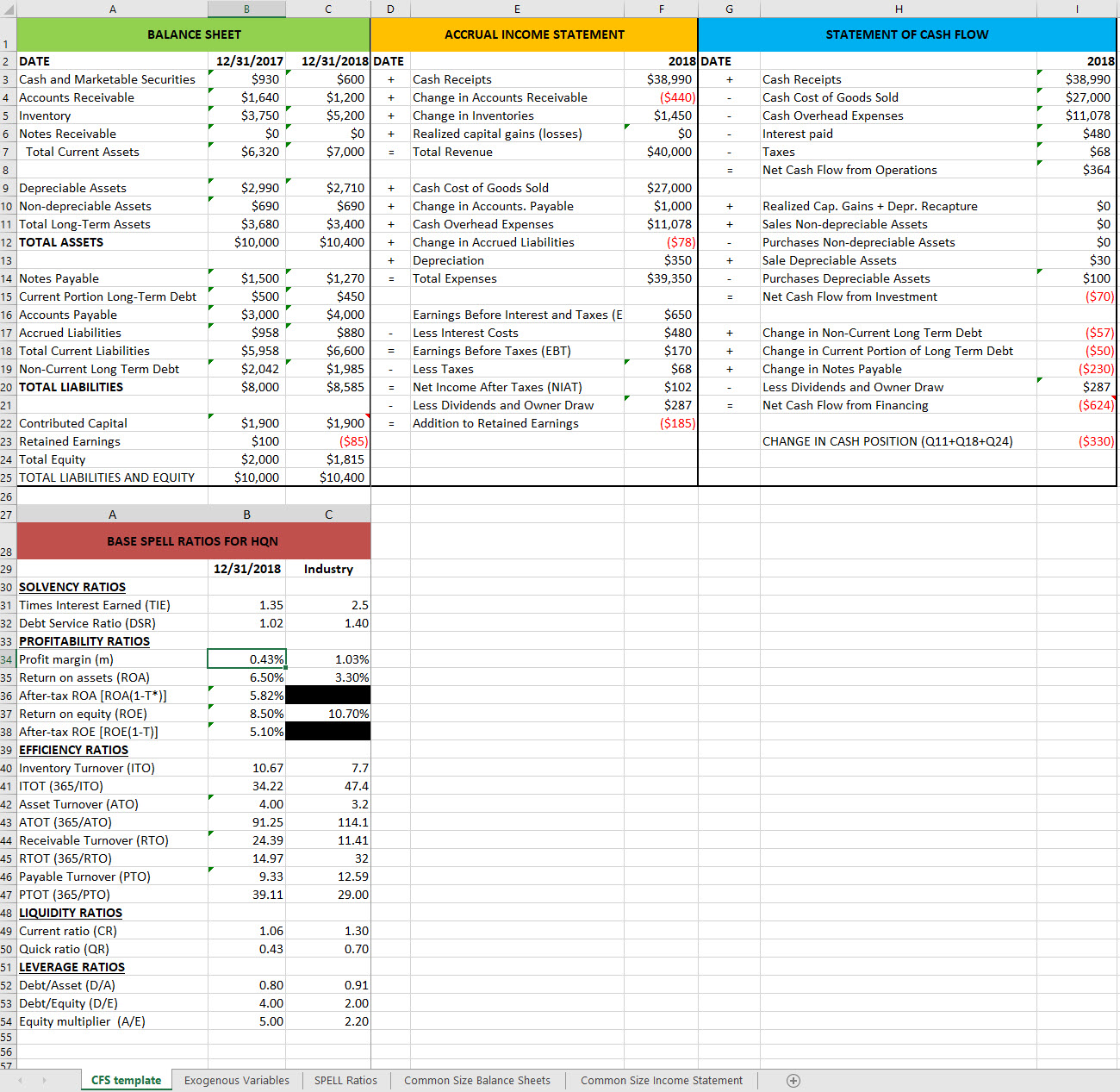

Chapters in Part II focus on the internal financial strengths and weaknesses of the firm and its ability to respond to external opportunities and threats. Chapter 5 focuses on the construction, analysis, and interpretation of coordinated financial statements (CFS). CFS are the primary tools for answering the question: what is the financial condition of the firm and what are its financial strengths and weaknesses?

An important consideration, especially when the focus is on small to medium-sized firms, is how to construct financial statements when the firm has incomplete records. While the data used in the financial management process and the construction of financial statements are most often assumed to be obtainable and accurate, the reality may be quite different. Small to medium-sized firms often lack the financial records required to conduct the analyses described in Part II of this book. Acquiring and sometimes guesstimating the missing data is almost an art form—a process that forms the nexus between theory and practice.

An important lesson to be learned about financial statements—even when we can construct them accurately—is that financial statements alone do not completely reveal the financial strengths and weaknesses of the firm. A more complete view of the firm’s strengths and weaknesses requires ratios be constructed using data included in the firm’s CFS (Chapter 6). Ratios constructed using the firm’s CFS can be compared with similar firms, and significant deviations from the norm can be noted and given further attention. Ratios describing the firm’s financial well-being can be described by the acronym SPELL: (S)olvency, (P)rofitability, (E)fficiency, (L)iquidity, and (L) everage.

Chapter 7 notes that the firm’s CFS is a system. An important characteristic of an open system is that its parts are connected internally with endogenous variables and externally—to factors outside of the firm—with exogenous variables. Therefore, a change in one or more of the firm’s exogenous variables can change conditions inside the firm described by its endogenous variables.

Because CFS are a system, we can analyze the firm’s opportunities and threats presented by forces outside the firm. For example, we can ask: what if there is a change in the firm’s exogenous variables? Then, how will the financial condition of the firm change? Or we may ask: if the firm has a financial goal, then how much must an exogenous variable change for the firm to reach its goal? Finally, we may ask: if one part of the system changes, what will be the corresponding change? One way to think of the CFS system and what if and how much analysis is to compare it to a balloon: a squeeze somewhere in the balloon will produce a bulge somewhere else.

Throughout this book, we use data from a hypothetical (but not atypical) firm, HiQuality Nursery (HQN) to help make the analysis realistic. However, the financial analysis experience becomes authentic when those practicing financial management skills construct financial statements for actual firms, including ones in which the analyst has a personal interest.

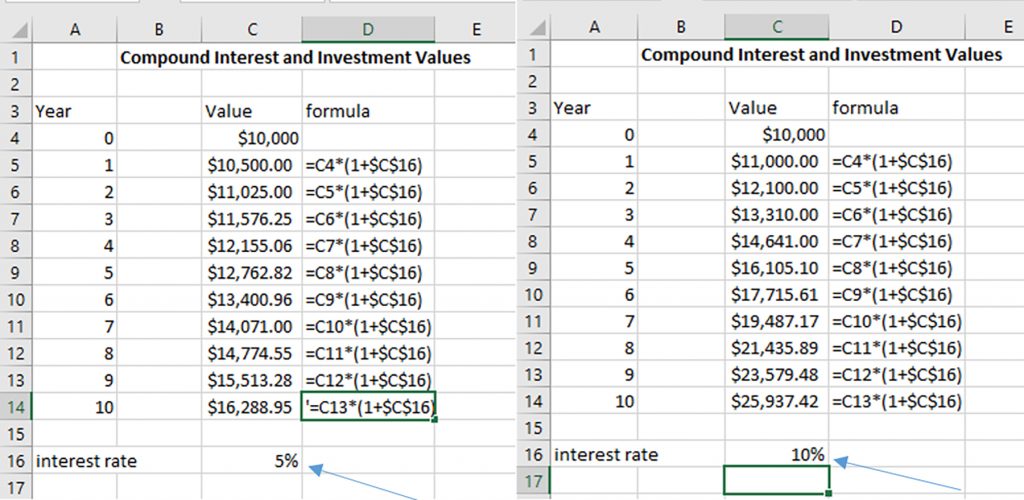

Chapters in Part III of this book introduce present value (PV) models. Chapter 8 provides the theoretical basis for PV models by demonstrating that PV models are multi-period extensions of a single period accrual income statement (AIS). To aid those preparing PV models, this chapter also introduces a generalized Excel template that can be used to solve practical PV problems. While PV models have the common feature of converting a challenger’s future cash flow to its equivalent in the present, Chapter 9 introduces several different kinds of PV models distinguished by the questions they answer. Chapter 10 introduces one important distinction between PV models, whether the investment is an incremental change to an existing firm versus a stand-alone investment. Chapter 11, the last chapter in Part III of this book, describes forecasting methods useful for obtaining future cash flow estimates to populate PV models. Included in chapter 11 is a brief introduction to statistical regression methods, essential for forecasting.

Chapters in part IV provide more detailed guidelines for constructing PV models. Chapter 12 compares a challenging investment to a defending one by converting a challenger’s future cash flow to its equivalent in the present by exchanging cash flow between periods at the defender’s internal rate of return. Chapters 13, 14, and 15 remind those solving PV problems that comparisons between challenger(s) and defenders(s) must use homogeneous measures. Chapter 13 describes how to compare investments with different sizes. Chapter 14 describes how to compare investments with different terms. Chapter 15 describes how to introduce taxes into PV models to produce consistent comparisons between challengers and defenders. Finally, chapter 16 introduces homogeneous currency and liquidity requirements when comparing challenging and defending investments.

Armed with a knowledge of PV model building principles and tools, the analyst is prepared to construct PV models for specific investments. Chapters in Part V note that specific investments, while similar, may have some distinct characteristics, depending on the type of investment activity under examination. Chapter 17 considers taking out and repaying loans, emphasizing that loan analysis is essentially a present value problem. Chapter 18 considers purchasing, using, or selling land. An important feature of land purchases and sales is transaction costs, which are included in the land models. Chapter 19 recognizes that the control and use of investments can be acquired through leases as well as through purchases. So, in this chapter, models are constructed that can be used to find the present values of leases. Chapter 20 reviews financial investments, a separate class of investments, especially relevant for personal financial management decisions. Chapter 21 prepares students to observe financial opportunities and threats using the term structure of interest rates, an important financial tool. Finally, Chapter 22 reminds readers that “money can’t buy love” nor most other relational goods. Thus, Chapter 22 enlarges the management process to include relational goods as well as commodities.

To solve many of the problems in this text, we employ Excel spreadsheets that are now generally available and which have become the “industry standard” for solving financial management problems. Excel spreadsheets enable the analyst to solve complicated financial problems and examine the robustness of a solution under different possible scenarios. Although students are expected to come to this class with Excel experience, we include in this book an Appendix that provides a brief review of Excel methods employed in this text. Chapter 7 includes an appendix to explain the HQN Coordinated Financial Statement Excel template. Chapter 8 includes an appendix to explain the Green & White Services PV Excel template. Chapter 11 includes an appendix showing how to manage Excel add-ons to access the Data Analysis option.

Finally, throughout this text we identify paragraphs that summarize key concepts explained in the preceding material. These key paragraphs are shaded to suggest that the reader pay them particular attention.

7

The authors thank Julie Taylor for bringing the material in this text to publication and for making it available as an Open Education Resource (OER) book. Julie is a library assistant at the Michigan State University Libraries and is responsible for its publishing services where this text is printed. She has edited, organized, formatted, and printed this text. Without Julie’s direction, patience, persistence, wit, and wisdom, this book would have undoubtedly gotten lost in its many revisions. Thank you, Julie.

We thank Larry Borton for providing relevant and current tax code details included in Chapter 3.

Thanks also go to the Department of Agricultural Food and Resource Economics (AFRE) at Michigan State University (MSU) for the support needed to write this text and the many students in the Agricultural Business Management 435 (ABM 435) classes whose feedback helped shape the content and the presentation of materials included in this text.

Some of the chapters in this book were adapted from published articles and books written by the authors of this text and co-authors. We acknowledge these contributions in footnotes in the chapters in which their contributions appear.

I

1

Learning goals. After completing this chapter, you should be able to: (1) recognize the six steps included in the management process; (2) apply the management process to better manage the financial resources of the small to medium-size firm; and (3) apply the management process to other activities such as being a successful student.

Learning objectives. To achieve your learning goals, you should complete the following objectives:

Financial management is about, above all else, management. The verb manage comes from an Italian verb meaning “to handle” as in how a rider handles a horse. The management process can be applied to a wide variety of organizations and resources. In this book, we apply the management process to managing the financial resources of the small business as opposed to larger corporations.

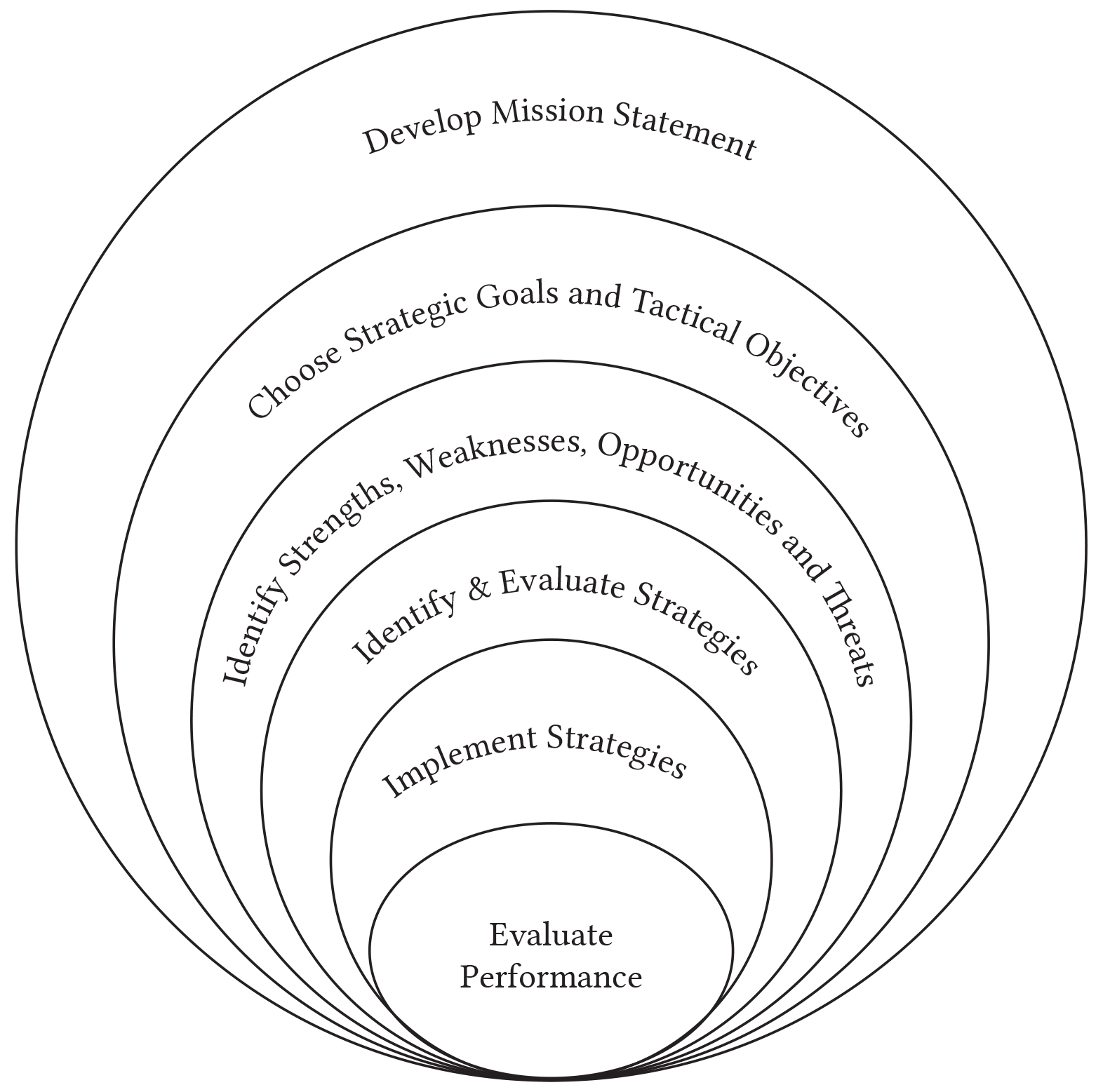

The management process includes six steps: 1) develop the firm’s mission statement; 2) choose the firm’s strategic (long-term) goals and tactical (short-term) objectives; 3) identify the firm’s strengths, weaknesses, opportunities, and threats; 4) develop the firm’s strategy for accomplishing its strategic goals and tactical objectives; 5) implement the firm’s strategy; and 6) evaluate the firm’s performance.

These six steps are illustrated in Figure 1.1 followed by narrative that describes them in more detail. Note that as one moves from one management step to the other, one moves toward the center of the circle in Figure 1.1. And as one moves toward the center of the circle, each activity is constrained by previous management choices.

The management process begins with a mission statement. The firm’s mission statement explains why the firm exists and what it values. The mission statement may also establish criteria for selecting activities in which the firm will participate. Mission statements might also describe the firm’s customers, the markets in which it will participate, and the firm’s social responsibilities. Mission statements are often succinct, short, easy to express and remember, clear, and flexible enough to describe the entire range of the firm’s activities. For example, a mission for a vegetable farm may be: “our mission is to provide wholesome and safe vegetables grown in an environmentally healthy and worker-friendly environment.”

Motives play a critical role in the formulation of the firm’s mission statement. Motives spring from physical and socio-emotional needs and the relative importance of these motives will determine how the firm manages its resources to satisfy its needs. Therefore, the relative importance of the financial manager’s motives should be reflected in the mission statement. To illustrate, motives may reflect the need to increase one’s own consumption, to act in accordance with one’s internalized set of values, to earn the good will of others, to increase one’s sense of belonging in one’s community or other organizations, and to improve the well-being of a disadvantaged group. The mission statement needs to guide the firm’s efforts to manage its resources depending on the relative importance of these competing motives.

One word sometimes associated with management is the word “vision.” Vision is the ability to imagine or picture, in one’s mind, something that has not yet been created physically. Therefore, vision is a necessary condition for any kind of physical creation because we must create an event, outcome, or thing in our mind before we can create it physically. An architect must imagine a building and reflect that vision in plans which the builders will follow to create a building. A football coach imagines an offensive play and reflects it in a drawing before it can be executed in a game. A financial manager must imagine a project that will produce valued outcomes before committing time, energy, and other resources to the project. A vision of what the manager wants the firm to achieve is reflected in the firm’s mission statement. A biblical expression highlights the importance of vision: “where there is no vision, the people perish…” (Proverbs 29:18).

Strategic goals set the long-term direction of the firm. Strategic goals are consistent with the firm’s mission statement—what it values, why it exists, and what is its purpose. Strategic goals direct the firm’s efforts toward achieving its mission over the long run. Strategic goals also call for tactical objectives, specific actions needed to achieve strategic goals. For example, a strategic goal may be to increase the firm’s revenues by 10%. The objectives consistent with this goal may be to develop new products, to focus on a marketing strategy, or to increase the firm’s sales force. The firm’s objectives transform the firm’s strategic goals into an action plan. Tactical objectives describe what short term actions are required if the firm is to reach its long-term goals.

There are at least four reasons management requires the firm to choose goals and objectives:

Some goals are better than others. The four reasons why we choose goals and objectives help us define the characteristics of good goals and objectives.

Before developing strategies to accomplish the firm’s goals and objectives, a manager needs to identify and evaluate the internal strengths and weaknesses of the firm. This evaluation should include an assessment of the firm’s ability to survive financially in both the long run and the short run (solvency and liquidity); its profitability; its efficient management of its resources on which its profitability depends; and the risk inherent in its current financial state. External opportunities and threats that impact the firm’s ability to accomplish its objectives also need to be considered. An external opportunity and threat analysis might include evaluating the behavior of close competitors or assessing the condition of the economy and business climate, or the impacts of the business cycle on clients’ incomes and the resulting product demand.

The firm’s strategy is a plan that describes how it intends to achieve its strategic goals and its tactical objectives. Some have claimed that a goal or objective without a plan is only a wish. The firm’s strategy is a plan of action that describes who will do what, when, and how. For each goal or objective, the firm must develop the corresponding strategy to accomplish it. The strategy development process includes collecting data and information about possible choices and likelihoods of possible events. Then, the information must be analyzed to determine the impact of a strategy on the firm’s goals and objectives. Based on these analyses, management must select the proper strategy.

Once a strategy is selected, it must be administered throughout the firm. All relevant parts of the business (accounting, purchasing, manufacturing, processing, shipping, sales, administration) must support and take an active role implementing the strategy. There may be changes in the business that are necessary to implement the strategy such as changes in personnel, technology, or financial structure. Implementing the firm’s strategy will require a carefully coordinated effort if the firm’s strategy leads to the firm achieving its goals and objectives.

Firm managers must continually evaluate the strategies they implemented to reach the firm’s objectives and goals. They must determine if what the firm has achieved is consistent with its mission statement, goals, and objectives within an environment described by the firm’s strengths, weakness, opportunities, and threats. Firm managers must also be prepared to alter strategies in response to changes in technologies, laws, market conditions, and personnel. These changes will make it necessary for the firm to continually reevaluate and adjust.

Evaluating the firm’s performance must also include a review of its mission statement, goals, objectives, efforts to implement its strategies, and its strengths, weaknesses, opportunities and threats. Since the firm’s mission statement and strategic goals are oriented toward the long term, they change infrequently. However, the firm’s strategies may change as frequently as its internal strengths and weaknesses and external opportunities and threats change.

The firm’s financial management process involves the acquisition and use of funds to accomplish its financial goals and objectives consistent with its financial mission statement. The firm’s financial management process essentially employs the same six management steps described earlier. The six steps of financial management include: 1) develop the financial mission of the firm; 2) choose the financial goals and objectives of the firm; 3) identify and evaluate the firm’s financial strengths, weaknesses, opportunities and threats; 4) develop financial strategies including evaluating and ranking investment opportunities to achieve financial goals and objectives consistent with the firm’s mission; 5) implement investment strategies by matching the liquidity of funding sources with cash flow generated from investments, by forecasting future funding needs, and by assessing the risk facing the firm; and, 6) evaluate the firm’s financial performance relative to the goals and objectives of the firm. These six steps are described next in more detail.

While financial management usually plays a role in developing the firm’s overall mission statement, there are other considerations shaping the firm’s mission. As a result, the financial mission of the firm is usually nested within the more general mission of the firm. One financial mission of the firm may be to reach certain financial conditions that allow the firm’s owners to pursue other goals and provide firm owners resources in the future. The firm’s mission statement may lead naturally to important financial goals such as to maximize profit, reduce costs and increase efficiency, manage or increase the firm’s market share, limit the firm’s risk, or maximize the owner’s equity in the firm. However, there may be a distinction between a firm’s financial mission and the firm’s overall mission. In other words, the firm’s financial mission included in the strategic financial management process may be an objective in the firm’s overall strategic management process.

The part of the firm’s mission related to financial management must lead to the firm selecting financial goals consistent with the firm’s mission statement and objectives likely to lead to the successful achievement of its strategic goals. The financial objectives may direct how the firm organizes itself, how it manages its tax obligations, and how it responds to risk—subjects discussed in Chapters 2, 3, and 4.

The use of coordinated financial statements (CFS) discussed in Chapter 5 can be used to evaluate the firm’s internal strengths and weaknesses. We may need to look outside of the firm to identify external opportunities and threats facing the firm. Financial statements are used to formulate ratios that can be compared to other firms to determine how the firm’s financial condition compares to normal—or average—firms, the subject of Chapter 6. Chapter 7 uses financial statements and ratios to demonstrate that the firm is a system with interconnected parts. As a result, each financial measure (e.g. solvency, profitability, efficiency, liquidity, and leverage) are connected to each other, and a change in one measure will change all the others.

Financial managers face an almost limitless set of investment opportunities with a wide variety of characteristics. Some investments will be liquid and easily converted to cash, such as inventories or time deposits. Other investments, such as real estate or production facilities, cannot be easily converted to cash and are considered illiquid. There are investments that provide fairly certain, low risk returns while others will provide uncertain, high risk returns. Some investments are depreciable while others increase in value over time. Firm budget resources for capital or long-term investments and evaluate them using present value (PV) tools. Many of the chapters that follow focus on PV models. Indeed, it may be correct to say that the focus of much of this book is on how to use PV models to evaluate a firm’s financial strategy.

Equipped with PV models and knowledge of how to conduct proper comparisons of investments using consistent measures, we are prepared to apply our tools to a wide range of investment problems that employ a variety of PV models. Included is a discussion of loan analysis in Chapter 17, land investments in Chapter 18, leasing options in Chapter 19, and investment in financial assets in Chapter 20. Then Chapter 21 introduces yield curves to help us identify outside-of-the-firm external threats and opportunities. Finally, the last chapter in this book, Chapter 22, ends with a cautionary note—there are relational goods that may be more important than money and should not be ignored.

Financial managers often play an important role in managing the implementation of an investment strategy. The implementation stage of financial management may include interacting with capital markets to raise funds required to support a strategy. Managers decide whether to acquire funds internally or borrow from other investors, commercial banks, the Farm Credit System, life insurance companies, or, depending on how the firm is organized, by issuing stocks or bonds.

In the process of obtaining and allocating funds, financial managers interact directly or indirectly with financial markets. This interaction could be simply obtaining a savings or checking account at your local bank. Or it could involve more sophisticated interactions such as raising funds by issuing ownership (equity) claims in your firm in the form of shares of stock.

Another part of implementing the financial strategy of the firm is to interact with various parts of the business and the household. For example, setting inventory policy is both a financial and business management decision and requires input from the production and sales departments of the firm as well as the firm’s financial managers. In addition, financial managers must make trade-offs between risks and expected returns. One tool that can be used to evaluate future returns and risk is the term structure of interest rates, the subject of Chapter 21. There are other kinds of trade-offs as well. One important trade-ff is between commodities and relational goods. We will need both because they each satisfy different needs. This book is mostly about managing commodities, but Chapter 22 reminds us that “money can’t buy love” or relational goods. Therefore, one more thing about management is to account for and manage relational goods.

Finally, financial concepts and information are often used to evaluate a strategy’s performance and to signal investment changes the firm needs to adopt in the future. In this effort, PV models will prove to be particularly helpful.

The relative importance of the six steps included in the management process will differ depending on what is being managed. In the case of financial management, the financial goals, the objectives, the strengths, weaknesses, opportunities, and threats analysis, and the strategies adopted and evaluated will differ from personnel management, for example. Like both financial management and other management efforts is their shared responsibility for the firm. What follows is strategic firm management applied to the financial resources available to the firm.

Our focus on firm financial management. While all six firm financial management processes are important and discussed in this book, we focus on two:

Of course the other parts of the management process are important, especially implementing strategic financial investment plans and evaluating the firm’s performance. However, a thorough treatment of these topics which should be pursed in other venues.

Of course, the other parts of the management process are important, especially implementing strategic financial investment plans and evaluating the firm’s performance. However, a thorough treatment of these topics is better pursued in other venues.

The firm’s financial goals and objectives guide the financial manager. There are, of course, a wide range of possible tactical objectives that a firm may adopt to achieve its strategic goals and its mission. However, one maxim should guide the manager’s choice of objectives: “There is no such thing as a free lunch!” Interpreted, this adage reminds us that nearly always, every objective comes at the cost of another objective

For example, consider the objective of maximizing the firm’s profits. Increases in short-term profits may often reduce long-term profits. If the firm desires to reduce its risk, this may require that the firm reduce its profits by investing in less risky–but lower return–investments.

One often-stated firm financial management objective is to maximize the profits of the firm. However, the measure of profits can differ drastically across different accounting practices. For example, cash versus accrual accounting, different depreciation methods, and different inventory accounting methods all lead to different measures of profit. Maximizing profits using one accounting method may not maximize profits using another accounting practice. Furthermore, profits may be difficult to measure when the firm employs unpaid family labor. The real problem is that profits don’t reflect the actual cash flow of the firm.

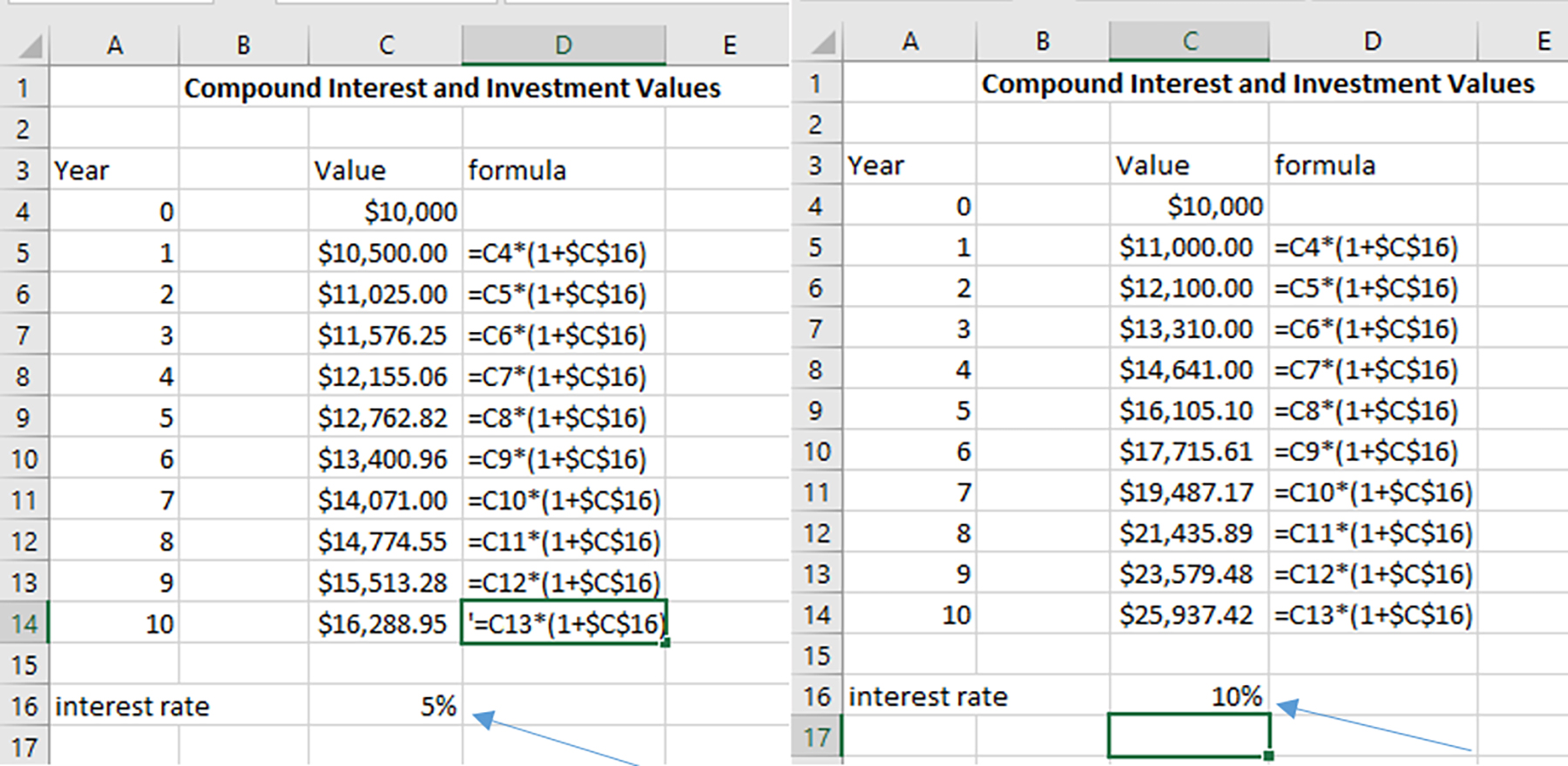

In addition, the traditional notion of profit ignores the timing of the cash flow received by a firm. Suppose you are given the choice of receiving $1,000 either today or one year from today. Which would you choose? Naturally, you would choose to get the money today because you could invest the money for some positive rate of return and earn more than $1,000 by the end of one year. For instance, suppose you could invest the money in the bank and earn a 5 percent return during the year. At the end of the year you would get back your $1,000 plus $1,000 x (.05) = $50 interest or a total of $1,050. Clearly, the $1,000 today is worth more than the $1,000 one year from today. The notion that dollars at different points in time are not worth the same amounts at a single point in time is known as the time value of money concept. Moreover, it underlies one of the most important financial trade-offs: present profits versus the present value of discounted future after-tax cash flow.

Another trade-off involving the maximize profit objective is that it ignores liquidity. Liquidity can be defined as a firm’s ability to meet unexpected cash demands. These cash demands might be unexpected cash expenses for such things as repairs and overhead expenses, new investment opportunities, or unexpected reductions in revenue. The concept of liquidity is closely related to risk. Liquidity needs are usually met by holding salable assets and/or maintaining the capacity to borrow additional funds. Serious risks may reduce the value of some assets and make liquidation of the assets difficult. Likewise, serious risk may also make it difficult to borrow additional funds.

If you were a firm manager, would your objective be to maximize profits or would some other objective be preferable? In this class, we will argue that traditional profit maximization is not a very desirable objective for a financial manager. We will argue that in most cases, financial decisions should be made so they maximize the value of the firm, which turns out to be the same thing as maximizing the present value of all the future cash generated by the firm. Once again, it is important to note that “cash flow” is much different than “profit.”

This concept of maximizing firm value is easy to defend in large firms where firm ownership is often separate from management. Owners of these firms generally want management to operate the firm in a way that maximizes the value of their investment; however, in smaller firms and households the value maximization principal is often constrained by other considerations such as concerns about quality of life. For example, you would likely be able to increase your personal wealth over time by driving a Chevrolet instead of a Cadillac (you could invest the cost savings), but you may gain enough satisfaction from driving a Cadillac (or a tractor with green paint) that you are willing to accept the lower wealth level. Nevertheless, for most of this course we will assume that financial decisions are made in a manner that is consistent with maximizing value. In cases where a firm does not maximize present value, it is still useful to estimate the present value maximizing decisions as a benchmark in order to understand the cost of alternative decision in terms of wealth loss.

Like it or not, we are all managers—if not managers of a firm then we are personal managers. We have important management responsibilities for our lives and resources. The management process is a universal process requiring that we first determine our mission and what goals and objectives are consistent with our mission? The goals and objectives we choose must declare what it is that we believe we can and should accomplish and the level of our commitment to reaching our goals and objectives. Finally, we cannot avoid setting goals and objectives because having no goal or objective is a goal or objective—to reach nowhere in particular.

Choosing our goals and objectives is crucial in the management process. We cannot achieve our mission without properly formulated goals and objectives. Goals and objectives lead us to conduct an honest evaluation of our internal strengths and weakness and external threats and opportunities, a process that identifies the resources and constraints likely to contribute to achieving our mission. After formulating our goals and objectives, and after conducting an honest evaluation of our strengths, weaknesses, opportunities and threats, we next decide on a strategy, a plan to follow that will enable us to accomplish our mission. Strategic management requires that we implement our plan, that we take specific actions to ensure we achieve our goal by implementing our strategies. And finally, we evaluate and, if necessary, modify our goals, objectives, and our understanding of our strengths, weaknesses, threats, and opportunities. Then, when we have completed the management process, we repeat it all over again, continually, and not necessarily following the steps in the management process in the same order. We end this chapter by emphasizing this truism: we are all managers, all the time.

Monson, T.M. (1970). “Thou Art a Teacher Come From God,” Conference Report, Oct. 1970, 107.

2

Learning goals. After completing this chapter, you should be able to: (1) know the different forms of business organizations; (2) compare the advantages and disadvantages of alternative business organizations; and (3) identify how alternative business organizations can influence a firm’s ability to achieve its financial goals and objectives.

Learning objectives. To achieve your learning goals, you should complete the following objectives:

The way a business is organized influences its ability to reach its goals and objectives. This chapter focuses on legal forms of business organizations that are widely used in the U.S. These include sole proprietorships, general and limited partnerships, limited liability corporations (LLCs), S corporations, and C corporations. Partnerships, LLCs, and C corporations are found across a wide spectrum of business types and sizes. LLCs are becoming increasingly important in the production agricultural sector, particularly with multi-generation family businesses. In family businesses, legal business structures which facilitate intergenerational transfer of assets has become particularly important.

Characteristics of businesses organizations that influence the ability of a firm to reach its goals and achieve its mission include: 1) who makes the management decisions; 2) how much flexibility does it have in its production, marketing, consumption, and financing activities; 3) its liability exposure; 4) its opportunities for acquiring capital; 5) how the life of the business is defined; 6) how the death of its owners affects the firm; 7) methods available for transferring the current owners’ interest to others; and 8) Internal Revenue Service definitions of business profits and their taxation. Thus, the way a firm is legally organized provides the framework for making financial management decisions.

The sole proprietorship is a common organization form especially used by small businesses. A sole proprietorship is a business that is owned and operated by a single individual. Most sole proprietorships are family-owned businesses. The advantages of a sole proprietorship business include:

The disadvantages of the sole proprietorship include:

Sole proprietorships are typically organized informally and require relatively little paperwork to begin operations. It is the most simple among the alternative business organizations to understand and use. To begin operation, the individual declares himself/herself to be a business. In many cases, a license will be required to operate the business, but often the business begins simply by “opening its door.” The day-to-day operations of the firm are also organized informally and may be administered as the owner desires, subject to legal and tax restrictions. For example, certain taxes must be paid by specific dates. The vast majority of regulations small businesses face are independent of the legal form of the business. Metrics such as business size, number of employees, and location often determine which regulations businesses face.

Since sole proprietorships are owned by a single individual, this form of business organization offers the maximum management control. In small firms, the owner of the business is often involved in all aspects of the business: purchasing, inventory control, production, sales, accounting, personnel and customer relations, as well as financial and general management. While the large amount of owner control can be a strength in small firms, it often turns out to be a disadvantage as firms begin to grow and the owner is no longer able to manage all aspects of the business. The owner must then hire competent staff to manage specific aspects of the business.

Sole proprietor business resources equal those available to the owner. This can restrict the startup of the business as well as its growth over time. In many cases, substantial cash outlays are required to make the capital purchases (land, facilities, equipment, cars, offices) to start the business and to provide initial overhead expenses (salaries, wages, supplies) until the business gets going. Further, it frequently takes two or three years before the business begins to show a profit. The owner of the business has to obtain these funds using their own equity (funds owned by the individual) and/or by borrowing funds, and borrowing requires collateral in the form of owner equity The amount that can be borrowed depends on the equity as well as the projected cash flow generated by the business. The lack of available financial capital for starting and expanding the business is a major drawback of the sole proprietorship. The profits from the business are taxed as personal income to the owner.

Sole proprietorships are subject to unlimited liability which means that the liability for business debts extends beyond the owner’s investment in the firm. For example, if the sole proprietorship is unable to cover its debts and obligations, creditors have the right to collect the personal assets that are not part of the business or other businesses of the owner. The owner may be forced to liquidate assets, such as a personal savings account, a vacation home, or other personal assets just to cover the firm’s obligations.

Another disadvantage of a sole proprietorship is that it has a limited life that corresponds to life of the owner. The owner may sell assets from the business to another sole proprietorship or business. However, if the business is not terminated prior to the death of the owner, then after the proprietor’s death, the assets remaining in the firm will be distributed according to the owner’s will or comparable instrument. When the owner dies, the business is terminated.

A general partnership is a business that is owned and operated by two or more individuals. The partners contribute to the business, share in management, and divide any profit. Partnerships are usually created by written contract among the partners, but they can be legally recognized even without a written agreement. If the partnership owns real property, the partnership agreement should be filed in the county where the property is located.

Advantages of partnerships include:

The disadvantages of a general partnership include:

The advantages and disadvantages of a general partnership are similar to the sole proprietorship. Partnerships are generally easy and inexpensive to set up and operate administratively. Partnership operating agreements are critical. Like sole proprietorships, profit allocated to the partners is based upon their share in the business.

Managerial control resides with the partners. This feature can be an advantage or disadvantage depending on how well the partners work together and the level of trust in each other. Control by any one partner is naturally diluted as the number of partners increases. Partnerships are separate legal entities that can contract in their own name and hold title to assets

The challenge to partnerships extends beyond possible conflicts with the partners. Divorce and other disputes may threaten the survival of the partnership when a claimant to a portion of the business’s assets demands his/her equity.

Unlimited liability remains a strong disadvantage for a general partnership. All partners are liable for the debts of the firm. Due to this unlimited liability, the risks of the business may be spread according to the owners’ equity rather than according to their interests in the business. This risk becomes an actual obligation whenever the partners are unable to satisfy their shares of the business’s obligations.

Increasing the number of partners can increase the amount of capital that can be accessed by the firm. More partners tends to mean more financial resources and this can be an advantage of a partnership compared to a sole proprietorship. Still, it is generally difficult for partnerships to raise large amounts of capital—particularly when liability is not limited.

Ownership transfer and limited life continues to be a problem for partnerships; however, it may be possible to build provisions into the partnership that will allow it to continue operating if one partner leaves or dies. In some cases, parent-child partnerships can ease the difficulties of ownership transfer.

A limited partnership is another way businesses can organize. Limited partnerships have some partners (limited partners) who possess limited liability; limited partners do not participate in management of the firm. There must be at least one general partner (manager) who has unlimited liability. Because of the limited liability feature for limited partners, this type of business organization makes it easier to raise capital by adding limited partners. These limited partners are investors and make no management decisions in the firm.

One difficulty occurs if the limited partners wish to remove their equity from the firm. In this instance, they must find someone who is willing to buy their share of the partnership. In some cases, this may be difficult. Another difficulty is that the Internal Revenue Service (IRS) may tax the limited partnership as a corporation if it believes the characteristics of the business organization are more consistent with the corporate form of business organization.

In production agriculture, family limited partnerships serve a number of objectives. For example, parents contemplating retirement may wish to maintain their investment in a farm business but limit their liability and be free of management concerns. To reduce their liability exposure and be free of managerial responsibilities, parents can be limited partners in a business where younger family members are the general partner.

The joint venture is another variation of the partnership, usually more narrow in function and duration than a partnership. The law of partnership applies to joint ventures. The primary purpose of this form or organization is to share the risks and profits of a specific business undertaking.

A corporation is a legal entity separate from the owners and managers of the firm. Three fundamental characteristics distinguish corporations from proprietorships and partnerships: (1) the way they are owned and managed, (2) their perpetual life, and (3) their legal status separate from their owners and managers.

A corporation can own property, sue and be sued, contract to buy and sell, and be fined—all in its own name. The owners usually cannot be made to pay any debts of the corporation. Their liability is limited to the amount of money they have paid or promised to pay into the corporation.

Ownership in the corporation is represented by small claims (shares) on the equity and firm’s profit.

The two most common types of claims on the equity of the firm are common and preferred stock. The claims of preferred stockholders takes preference over equity claims of common stockholders in the event of the corporation’s bankruptcy. Preferred stockholders must also receive dividends before other equity claims. The preferred stockholders’ dividends are usually fixed amounts paid at regular intervals that rarely change. In most cases, preferred stock has an accumulated preferred feature. This means that if the firm fails to pay a dividend on preferred stock, at some point in time the corporation must make up the payment to its preferred stockholders holders before it can make payments to other equity claims.

Common stock equity claims are the last ones satisfied in the event of the corporation’s bankruptcy. These are residual claims on the firm’s earnings and assets after all other creditors and equity holders have been satisfied. Although it appears that common stock holders always get the “leftovers,” the good news is that the leftovers can be substantial in some cases because of the nature of the fixed payments to creditors and other equity holders.

Large corporations are usually organized as Subchapter C corporations.

The advantages of a C corporation include:

The disadvantages of a C corporation include:

Earnings from the corporation are taxed using a corporate tax rate. When earnings are distributed to the shareholders in the form of dividends, the earnings are taxed again as ordinary income to the shareholder. For example, suppose a corporation, whose ownership is divided among its 3000 shareholders, earns $1,000,000 in taxable profits for the year and is in a flat 40-percent tax bracket. Profits per share equal $1,000,000/3000—or $333.33. The corporation pays 40% of $1,000,000—or $400,000—in taxes to the government. Taxes per share equal $400,000/3000—or $133.33.

Now suppose the corporation distributes its after-tax profits to its 3,000 shares in the form of dividends. Each shareholder would receive a dividend check of $600,000/3,000 = $200. The $200 dividend income received by each shareholder would then be taxed as ordinary personal income. If all the shareholders were in the 30-percent tax bracket, then each would pay 30% of $200 or $60 in taxes, leaving each shareholder with $140 in after-tax dividend income.

So what is the total tax rate paid on corporate earnings? Dividing the taxes paid by the corporation and the shareholder by the profit per share, the total tax rate is ($133.33+$60)/$333.33 = 58%, a higher rate than would be paid on personal income of the same amount.

One of the primary strengths of the corporate form of business organization is that the most the owners of the firm (shareholders) can lose is what they have invested in the firm. This limited liability feature means that as a shareholder, one’s personal assets beyond the investment in the corporation can’t be taken to satisfy the corporation’s debts or obligations.

Ownership can easily be transferred by selling shares in the corporation. Likewise, the corporation has an unlimited life because when an owner dies, the ownership shares are passed to his/her heirs. The common separation of ownership and management in large corporations helps to ease the ownership transfer as the firm management process never ceases.

The easy transfer of ownership, separation of management and ownership, and limited liability features of a corporation combine to create a business structure that is designed to raise large sums of equity capital. Investors in large corporations don’t have to become involved in management of the firm. Their risk is limited to the amount of funds invested in the firm, and their ownership interest can be transferred by selling their shares in the firm.

Corporations are more expensive and complicated to set up and administer than sole proprietorships or partnerships. Corporations require a charter, must be governed by a board of directors, pay legal fees, and meet certain accounting requirements. Despite the relatively high setup cost, the primary disadvantage of the corporate form of business is that income generated by the corporation is subject to double taxation.

However, there is a limit on corporate earnings that are double-taxed. The corporation may pay reasonable salaries, and these are deducted from the corporation’s profits. Therefore, salaries paid to corporate workers and operators are not taxed at the corporate level. In some cases, the corporation’s entire net profit may be offset by salaries to the owners so that no corporate income tax is due. On the other hand, if the corporation pays dividends to the shareholders, those payments are subject to corporate-level income tax. However, the individual does not have to pay self-employment tax on the dividends. And, qualifying dividends (and most United States Corporation dividends can fit into this definition) are taxed at capital gains rates and not the individual’s top marginal tax rate. Finally, dividends paid to a shareholder that actively participates in the business are not subject to either the 0.9 percent Medicare surtax on earnings or the 3.8 percent tax on net investment income that are levied on higher-income taxpayers.

Another disadvantage of corporations has to do with the fact that the managers do not own the firm. Managers, who control the resources of the firm, may use them for their own benefit. For example, top management may build extravagantly large headquarters and buy fleets of jets and limousines for transportation. If less were spent on perquisites, then the income of the corporation would be higher. Higher income allows higher dividends to be paid to the owners (shareholder).

The (potential) self-serving behavior by management running contrary to the interests of stockholders is an example of a principal-agent problem. Methods of dealing with the principal-agent exist. One way is to hire auditors to monitor the use of firm resources. Further, a corporation has a board of directors responsible for hiring, evaluating, and removing top management. Boards are often ineffective because they meet infrequently and may not have access to the information necessary to fulfill their responsibilities. Additional problems exist if management personnel also sit on the board of directors.

Another way to deal with the principal-agent problem in corporations is to align the interests of management with those of shareholders. This is accomplished by basing the compensation of management on the value of the firm’s stock. A chief executive officer could receive stock options as a part of his/her compensation package. If the stock price rises, the value of the options increase, which benefits the manager financially. The shareholders also benefit when the stock price increases. Such an arrangement may reduce the principal-agent problem. However, very high executive compensation can often trigger criticism from external groups such as consumer or labor activists.

Limitations of linking management’s compensation to the value of its stock have been illustrated by Enron and Tyco corporations. These corporations inflated the value of their stocks and eventually bankrupted themselves and lost the investments of their employees. It seems there is still a lot to be learned about aligning the interests of corporate managers and shareholders.

Many small businesses, including farms, use the C corporation structure and operate much like partnership. This is frequently done for reasons of expensing and intergenerational transfer.

The corporation will need to be “capitalized” by some level of equity funds from the shareholders. It is common practice among lenders to require personal guarantees by the owners of small corporations before providing funds to the business. This essentially eliminates the limited liability features for those shareholders. As one might expect, due to these difficulties, many small corporations are not able to generate large amounts of capital by simply selling ownership shares. As a result, many small corporations do not really receive the full benefits of corporate organization but are still subject to the disadvantages, namely double taxation.

C corporations and S corporations. Any corporation is first formed under the laws of a particular state. From the standpoint of state business law, a corporation is a corporation. However, there are two types of for-profit corporations for federal tax law purposes:

There is an alternative form of corporate business organization that is often more desirable from a small business perspective. Subchapter S Corporations have limited liability protection, but the income for the business is only taxed once as ordinary income to the individual (Wolters Kluwer. n.d.).

Subchapter S Corporations are sometimes preferred by small businesses because they provide limited liability protection. Meanwhile the income for the business is only taxed once as ordinary income to the individual. There are requirements that must be satisfied for firms to be organized as Subchapter S corporations. These requirements include: (1) it cannot have more than 100 shareholders; (2) it may have only one class of stock; (3) it cannot have partnerships or other corporations as stockholders; and (4) it may not receive more than 20 percent of its gross receipts from interest, dividends, rents, royalties, annuities, and gains from sales or exchange of securities. In agriculture, these restrictions usually mean that only family or closely-held farm businesses can achieve Subchapter S status.

Federal income tax rules for Subchapter S corporations are similar to regulations governing partnerships and sole proprietors. However, corporations may provide certain employee benefits that are tax deductible. Accident and health insurance, group life insurance, and certain expenditures for recreation facilities all qualify. However, these benefits may be taxable to the employees and subsequently to the shareholders.

There is greater continuity for businesses organized under Subchapter S than for sole proprietorships or partnerships. Upon the death of shareholders, their shares of the corporations are transferred to the heirs and the Subchapter S election is maintained. Surveys suggest that the major reason farms incorporate is for estate planning. The corporate form allows for the transfer of shares of stock either by sale or gift. This is much easier than transferring assets by deed.

The Limited Liability Company (LLC) is a relatively new form of business organization. An LLC is a separate entity, like a corporation, that can legally conduct business and own assets. The LLC must have an operating agreement which regulates its business activities and the relationship among its owners (referred to as members). There are no restrictions on the number of members or the members’ identities. LLCs are subject to disclosure, record keeping, and reporting requirements that are similar to a corporation.

The attractive feature of the LLC is that all members obtain limited liability, but the entity is taxed as a general partnership. The LLC is similar in many respects to the Subchapter S corporation. The primary differences are: 1) the LLC has less restrictive membership requirements; and 2) the LLC is dissolved in the event of transfer of interest or death unless members vote to continue the LLC. Table 2.1 summarizes the primary characteristics of the business organizations discussed so far.

| Characteristic |

Organization |

||||||

| Sole Proprietorship | Partnership | Limited Partnership | S Corporation | C Corporation | Limited Liability Company | ||

| ownership |

|

|

|

|

|

|

|

| management decision |

|

|

|

|

|

|

|

| life |

|

|

|

|

|

|

|

| transfer |

|

|

|

|

|

|

|

| income tax |

|

|

|

|

|

|

|

| liability |

|

|

|

|

|

|

|

| capital |

|

|

|

|

|

|

|

A cooperative is a business that is owned and operated by member patrons. Generally, cooperatives are thought to operate at cost, with all profits going to member patrons. The profits are usually redistributed over time in the form of patronage refunds. Cooperatives often appear to operate as profit making organizations much the same as other forms of business organization. Agricultural cooperatives do not face the same anti-trust restrictions as non-cooperative businesses, and they enjoy a different federal income tax status. In most instances, the concepts and analysis techniques covered in this course will be relevant to financial management in cooperatives.

A trust transfers legal title of designated assets to a trustee, who is then responsible for managing the assets on the beneficiaries’ behalf. The management objectives can be spelled out in the trust agreement. Beneficiaries retain the right to possess and control the assets of the trust and to receive the income generated by the properties owned by the trust. Beneficiaries hold the trust and personal property, rather than title to the assets. The legal status of certain types of land trusts are unclear in some states.

Gross cash farm income (GCFI) includes income from commodity cash receipts, farm-related income, and government payments. Family farms (where the majority of the business is owned by the operator and individuals related to the operator) of various types together accounted for nearly 98 percent of 2.05 million U.S. farms in 2018. Small family farms (less than $350,000 in GCFI) accounted for 90 percent of all U.S. farms. Large-scale family farms ($1 million or more in GCFI) accounted for about 3 percent of farms but 46 percent of the value of production.

The USDA defines a farm as a place that generates at least $1,000 value of agricultural products per year. In 2007, farms generating between $1,000 and $10,000 of agricultural products made up 60% of the 2.2 million U.S. farms. Farms producing $500,000 or more in 2007 dollars generated 96% of the value of U.S. agricultural production.https://www.ers.usda.gov/data-products/ag-and-food-statistics-charting-the-essentials/farming-and-farm-income

Table 2.2 shows the percentage of farms by organizational type and their share of aggregate agriculture product sales according to the 2007 Census of Agriculture. Sole proprietorships are the dominant form of business organization measured by farm count (86.5%) but have only 49.6% of the value of agricultural production. Partnerships and family corporations make up 20.8% of farms but have 43% of the value of agricultural production. Non-family corporations, part of the “other organization” category, accounted for 0.4% of farms and 6.5% of the value of agricultural production.

| Business Type | % of Farms | % of Cash Receipts |

| Sole Proprietorships | 86.5% | 49.6% |

| Partnerships | 7.9% | 20.9% |

| Family CorporationsMore than 50% of the stock is owned by persons related by blood or marriage. | 3.95 | 22.9% |

| OtherNonfamily farms, estates or trusts, grazing associations, American Indian Reservations, etc. | 1.2% | 7.3% |

More generally, about 80 percent of all businesses (agriculture and non-agriculture) are organized as sole proprietorships while only around 10 percent of businesses are organized as corporations. Conversely, about 80 percent of business sales come from corporations while sole proprietorships account for only about 10 percent of business sales.

Recognizing that we cannot offer financial management tools that meet the needs of all business organizations, we purposely focus in this text on small to medium-size businesses. As a result, we focus on firms that depend on internal capital and exercise the maximum control of the firm.

3

Learning goals. At the end of this chapter, you should be able to: (1) describe the major components of the federal tax system; (2) know how the different forms of business organizations are taxed; (3) recognize the difference between marginal and average tax rates; and (4) understand how depreciation, capital gains, and depreciation recapture affect the amount of taxes a firm pays.

Learning objectives. To achieve your learning goals, you should complete the following objectives:

Chapter 2 proposed that one financial management objective is to organize the firm so that its value is maximized. Of course, “the firm” could mean any business organization ranging from a large corporate firm to a small business or even an individual household. Later, we will see that the firm’s value is determined by its after-tax cash flow, which can differ significantly from the firm’s profits measured by its accounting income. As a result, we need to understand the differences between a firm’s cash flow and its accounting income—this discussion will come later. Fortunately, for the most part, a detailed knowledge of specific accounting differences for the different types of business organizations isn’t essential for our purposes. So we begin by discussing some of the major components of the federal tax system that have a bearing on a firm’s after-tax cash flow.

Due to the influence of taxes on cash flow, it is important to have an understanding of how the tax system works. This chapter intends to present a few of the basic concepts related to taxes that are important from a financial management perspective. Our focus is on the federal tax code, because of its importance in determining after-tax profit and after-tax cash flow. Nevertheless, there are a number of additional taxes (e.g. state and local taxes) that can have a significant impact on a firm’s earnings and cash flow. It is important to consider the impacts of all taxes when making financial decisions. The federal tax laws are written by Congress. The Internal Revenue Service (IRS) is the agency responsible for administering the code and collecting federal income taxes. The IRS issues regulations which are its interpretation of the tax laws. The regulations are effectively the tax laws faced by businesses and individuals. One final word of caution: always remember that tax laws can and do change, and these changes are not always announced in ways that inform small businesses. Nevertheless, ignorance is not an excuse for incorrectly filing one’s taxes.

Individual (ordinary) tax liabilities are determined by subtracting certain allowable deductions from one’s total income to obtain taxable income. Taxable income is then used as the basis from which the tax liability is calculated. The general procedure is:

Gross income consists of all income received during the tax year in the form of money, goods and services, and property. Adjustments to income, including some past losses, may include income that is not taxed, such as interest income generated by nontaxable municipal bonds. Adjusted gross income may be reduced by subtracting personal exemptions and deductions regardless of whether you itemize or not and includes such things as business expenses and deductions for some types of Individual Retirement Account (IRA) contributions. A personal exemption is the allowable reduction in the income based on the number of persons supported by that income. You may claim deductions for yourself, your spouse, and other dependents who meet certain criteria. As of 2018, the personal exemption amount is zero until 2025. In addition, you can reduce your taxable income by either claiming a standard deduction or itemizing allowable expenses.

The standard deduction is an amount allowed for all taxpayers who do not itemize, and represents the government’s estimate of the typical tax-deductible expenses that you are likely to have. As of 2018, the standard deduction is $12,000 for single, $18,000 for head of household, and $24,000 for married filing jointly. These are adjusted annually for inflation. If your tax-deductible expenses are greater than the standard deduction, you can list them separately and deduct the total value of the itemized deductions. Itemized deductions include expenses for such things as medical expenses, certain types of taxes, mortgage interest expense, and charitable contributions. After reducing Adjusted gross income by subtracting Personal exemptions and deductions, we obtain our Taxable income, the amount of income that will be used to calculate your Tax liability.

The Federal income tax in the United States is called a progressive tax, meaning that the percentage tax rate increases as taxable income increases. In contrast, regressive taxes have their tax rate remain constant or decrease as taxable income increases. State sales taxes, property taxes, social security taxes, and in some cases, state income taxes are regressive taxes because as a percentage of one’s income paid as taxes they increase with a decline in one’s income.

Two different tax rate measures include the Average tax rate and the Marginal tax rate defined below:

average tax rate = tax liability / taxable income

marginal tax rate = tax rate on the next dollar of taxable income.

The average tax rate represents the “average” tax rate that is paid on each dollar of taxable income. The marginal tax rate is the tax rate that is paid on the next dollar of taxable income. In a progressive tax system, the marginal tax rate will always be equal to or greater than the average tax rate.

The federal tax rate schedule for 2018 taxable income is shown in Table 3.1.

| Tax Bracket | Married Filing Jointly | Single |

| 10% Bracket | $0 – $19,050 | $0 – $9,525 |

| 12% Bracket | $19,050 – $77,400 | $9,525 – $38,700 |

| 22% Bracket | $77,400 – $165,000 | $38,700 – $82,500 |

| 24% Bracket | $165,000 – $315,000 | $82,500 – $157,500 |

| 32% Bracket | $315,000 – $400,000 | $157,500 – $200,000 |

| 35% Bracket | $400,000 – $600,000 | $200,000 – $500,000 |

| 37% Bracket | Over $600,000 | Over $500,000 |

Due to the progressive nature of the tax, the marginal tax rate increases as your income increases. The first $19,050 of taxable income for married couples filing a joint return are taxed at a rate of 10%, the next $58,350 ($77,400 – $19,050) of taxable income are taxed at a rate of 12%, and so on. Suppose a married couple had $120,000 of taxable income in 2018.

Their Federal tax liability would be calculated on each increment of income as follows: The average tax rate paid equals Total tax liability/taxable income = $18,279/$120,000 = 15.2% and the marginal tax rate paid on the last dollar earned would be 22%.

10% tax on first $19,050 ($19,050 – $0) = 10% x $19,050 = $1,905.00

12% tax on next $58,350 ($77,400 – $19,050) = 12% x $58,350 =$7,002.00

22% tax on next $42,600 ($120,000 – $77,400) = 25% x $44,700 = $9,372.00

Total Tax Liability on $120,000 = $18,279.00

It is important to distinguish between the marginal and average tax rate. The average tax rate is useful because it allows us, with a single number, to characterize the proportion of our total income that is taxed. In many cases, however, we are interested in the amount of tax that will be paid on any additional income that is earned, perhaps as a result of profitable investment. In these situations, the marginal tax rate is the appropriate rate to use. For example, suppose your average tax rate is 18.4 percent and you are in the 22 percent tax bracket, and you receive a $1,000 raise. The additional income you earn will be taxed at the marginal tax rate of 22 percent, regardless of the average tax rate, so that your increase in after-tax income is only $1,000(1 – .22) = $780. The marginal tax rate is also significant when considering the impact of tax deductions. Suppose you are in the 22 percent tax bracket and you contribute $2,000 to your favorite charity. This reduces your taxable income by $2,000, saving you $440 in taxes (22% times $2,000) so that your after-tax cost of your contribution is only $2,000(1 – .22) = $1,560.

As we pointed out earlier, because of the progressive nature of the federal tax code, the effective marginal rate that individuals pay is nearly always greater than the federal marginal tax rate. However, there are more levels of government collecting tax revenues than just the federal government. In addition to the federal tax, most personal income is also subject to state taxes, Social Security taxes, Medicare taxes, and perhaps city taxes. State taxes vary but often run in the 4 – 6 percent range. Social Security (6.2 percent) and Medicare (1.45 percent) taxes are split between employer and employee, and the rate for most employees is 7.65 percent (self-employed pay both the employer and employee half, usually 15.3 percent). In 2018, the social security tax is imposed only on individual income up to $128,400. There is no maximum income limit on the Medicare tax. City taxes can run 3 – 4 percent. Therefore, the effective marginal tax rate for someone in the 24 percent federal tax bracket who pays social security tax will generally be over 37 percent. If the same person were self-employed they would be subject to an additional 7.65 percent, and a marginal tax rate that could exceed 50 percent of taxable income in some cases. It should be noted that one-half of “self-employment tax” is deductible from income subject to federal tax, so the effective marginal tax rate increases by only 7.65(1 – .24) = 5.81 percent for someone in the 24 percent tax bracket. As you can see, it is extremely important to understand what the effective marginal tax rate is when making financial management decisions.

Progressive tax systems are subject to an undesirable feature, often termed “bracket creep.” Bracket creep is an inflation-induced increase in taxes that results in a loss in purchasing power in a progressive tax system. The idea is that inflation increases tend to cause roughly equal increases in both nominal income and the prices of goods and services. Inflation induced increases in income push taxpayers into higher marginal tax brackets, which reduces real after tax income. Consider an example of how inflation reduces real after-tax income and therefore purchasing power.

For the couple in our previous example with a taxable income of $120,000, their real after-tax income, their purchasing power in today’s dollars, is equal to their Gross income less any Tax liabilities which in their case is: $120,000 – $18,279 = $101,721. Another way to calculate their purchasing power is to multiply (1 – average tax rate T) times their gross income: (1 – 15.2325%)$120,000 = $101,721.

Inflation is a general increase in price. Suppose that, as a result of inflation, that next year inflation will increase your salary 10%. However, suppose that inflation will also increase the cost of things you buy by 10%. As a result, to purchase the same amount of goods next year that were purchased this year will require a 10% increase in this year’s expenditures. For the couple described in our earlier example, this will require expenditures of $101,721 times 110% = $111,893.10.

Now let’s see what happens to our couple’s after-tax income. A 10% increase in taxable income means they will have $120,000 times 110% = $132,000 in taxable income next year. Recalculating the couple’s tax liabilities on their new income of $130,000: